The Age Pension is designed to support the basic living standards of older Australians. It is paid to people who meet age and residency requirements. It is targeted through the means test to those who need it most. Pension rates are indexed to ensure they keep pace with Australian price and wage increases.

Most Age Pension payments are made by Services Australia (Centrelink). Age pensioners who also receive certain compensation payments from the Department of Veterans’ Affairs(link is external) (DVA) can choose to have their Age Pension paid by either DVA or Services Australia.

Age requirements

The pension age is being gradually increased from 65 to 67 years.

- 65 years and 6 months, if you were born between 1 July 1952 and 31 December 1953

- 66 years, if you were born between 1 January 1954 and 30 June 1955

- 66 years and 6 months, if you were born between 1 July 1955 and 31 December 1956

- 67 years, if you were born on or after 1 January 1957

Residence requirements

To qualify for the Age Pension, a person must be:

- an Australian resident (that is, living in Australia on a permanent basis) and

- in Australia on the day the claim is lodged

They must also satisfy one of the following:

- be an Australian resident for a total of at least 10 years, with at least 5 of these years in one period

- have a qualifying residence exemption

- be a woman who is widowed in Australia when both she and her late partner were Australian residents, and who has 104 weeks residence immediately before the claim

- be receiving Widow B Pension, Widow Allowance or Partner Allowance immediately before reaching pension age

Special rules apply to residence in countries with which Australia has an International Social Security Agreement. Residence in these countries may count towards the minimum 10-year residence requirement.

Means testing

The Age Pension is subject to an income test and an assets test. Pensioners are paid under the test that produces the lower rate of payment.

Income test

The pension income test is designed to encourage people to supplement their income support payments with other income, if they are able to. A pensioner can receive an amount of income before their pension starts to be reduced. This amount may comprise income from investments, earnings, or a combination of income from various sources and is known as the income free area.

For each dollar of income over the income free area, the single pension is reduced by 50 cents. For couples, their combined pensions are reduced by 50 cents. This means that for a pensioner couple, their individual pensions are reduced by 25 cents a fortnight for each dollar of income that the couple has over the income free area. To learn more about the pension income test, see the Services Australia website.

Assets test

The pension assets test is designed so that people with substantial assets use their assets (either directly or to produce income) to meet their day-to-day living expenses before calling on the social security system for support.

An asset is any property or possession that a person owns, with the exception of exempt assets. Where a person’s rate of pension is worked out under the assets test, the value of their assets above the assets free area reduces their pension by $3 a fortnight for each extra $1,000 in assets.

To learn more about the pension assets test, see the Services Australia website.

Deeming

The social security system uses deeming to assess income from financial investments. Deeming rules provide a simple and fair way to assess income from financial investments for social security and DVA pension and allowance purposes. On 1 January 2015, the deeming rules were extended to include account-based income streams. To learn more about deeming and these changes see the Services Australia website.

Rates

Pensions are indexed twice a year, on 20 March and 20 September. This reflects changes in pensioners’ costs of living and wage increases.

Base pension rates are indexed to the higher of the increase in the Consumer Price Index and the Pensioner and Beneficiary Living Cost Index. These measure changes in prices on a range of goods and services such as:

- food

- health care

- postage

- fuel

- housing costs

- utilities costs.

Following indexation to price increases, rates are compared to a wages benchmark, and increased to meet the benchmark if necessary. The wages benchmark ensures the couple combined rate of pension is at least 41.76% of Male Total Average Weekly Earnings.

The single rate of pension is 66.33% of the couple combined rate.

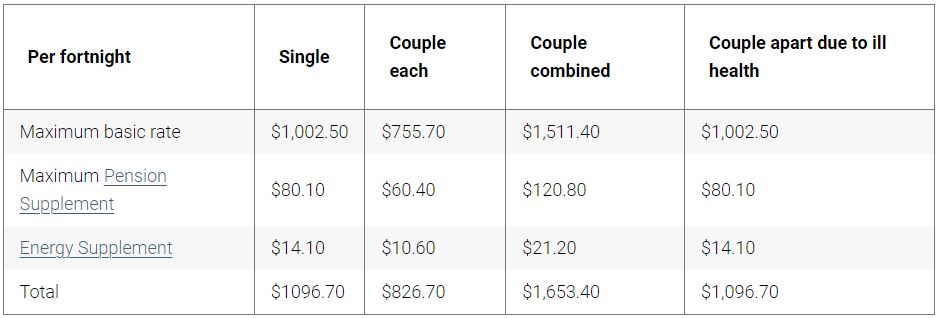

Normal rates

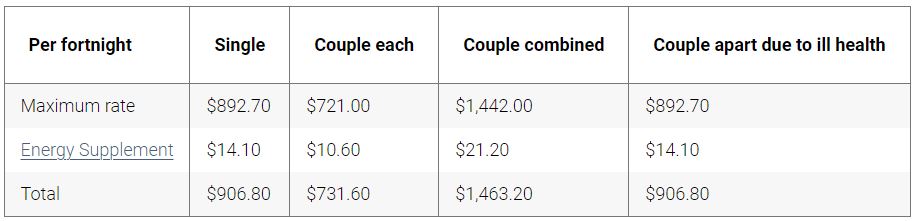

Transitional rates

Some people who were getting part pensions on 19 September 2009 are on transitional rates. This is until they catch up with the current normal rates.